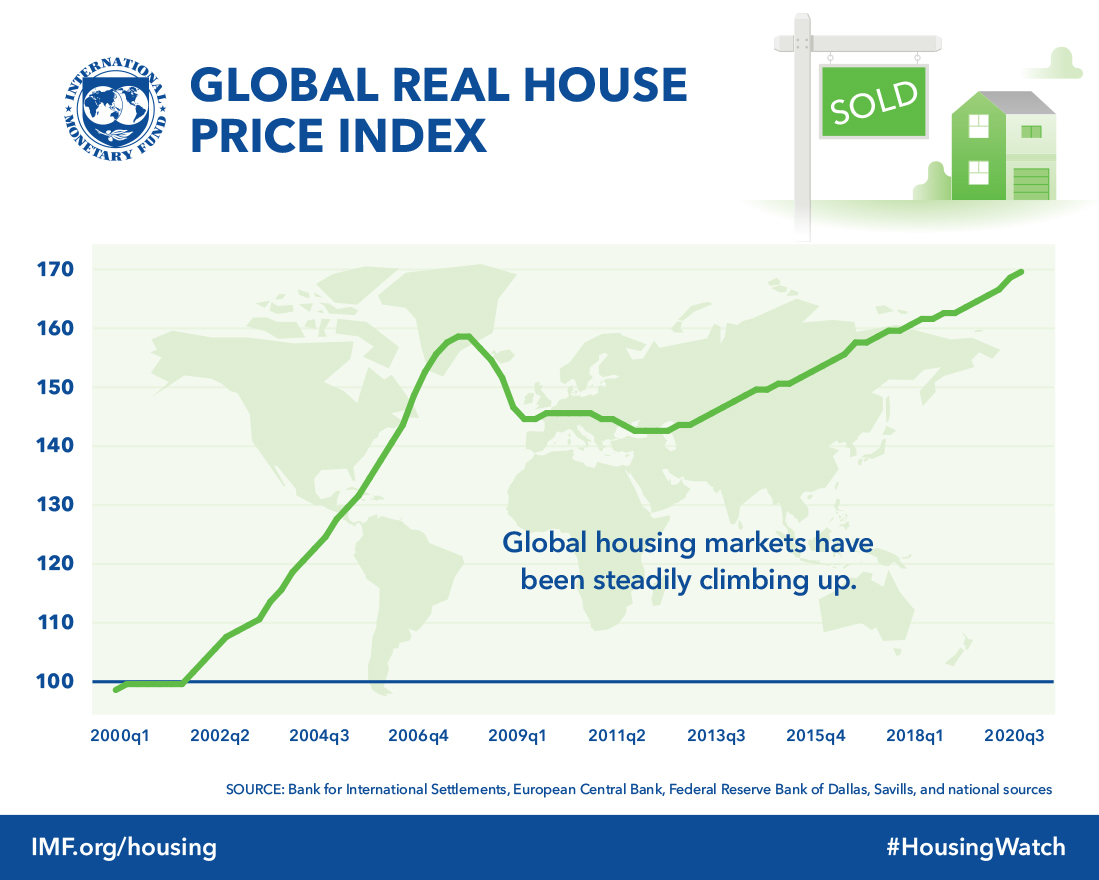

Some cautiously good news from the IMF as far as the global recovery is concerned.

Click here for article.

Nevertheless, I'm a slightly concerned about the volatility in the stock market amidst rising food, clothing, and

fuel costs in the US. These costly headwinds are immediately felt by families who are sticking to a budget (my family), and/or considering whether or not to spend money on possibly a new car or home.

Price stability is a responsibility of the Federal Reserve (hidden within their "dual mandate" of effectively promoting maximum employment and moderate long-term interest rates) and their record has not been a good one. My question to the Fed is "how can they have the responsibility to effectively keep prices stable - yet at the same time pursue "inflation targets", and quantitative easing schemes to "promote maximum employment"?

I don't know about you, but in the last 20 years it seems:

- things have become more expensive,

- more individuals need to have 2 or more jobs,

- less people can comfortably retire,

- college tuition is projected to be over $200,000 per child in 17 years from now according to The College Board SOURCES: The College Board, Annual Survey of Colleges; NCES, IPEDS,

- and families are becoming smaller (birthrate has declined).

All of the aforementioned items can be directly or indirectly linked to price instability, and minimum employment with possibly lower wages and longer hours. The rich get richer as they say...and the poor stay poor. But ask yourself - am I rich or poor today? Today, I am

neither.

So in 5 years from now (2019) - am I putting myself on the path to be richer? Or poorer? Because if I'm going to be richer in 5 years, then there's a good chance I'll be richer in another 5 years after that (2024)...because, as they say, the rich get richer. However, if I'm going to be poorer 5 years from now (or at least not doing anything to make myself richer) in 2019, then there's a good chance I'll be even poorer in another 5 years (2024) unless I stop the cycle.

I need another vehicle soon, and I don't just want any other vehicle - I

want a nice 2014 F-150 FX2 truck with dual exhaust or maybe a sport sedan like the Dodge Charger SRT8. But I know this is creating a monthly payment (liability) for myself and a monthly income (asset) for whatever car company I buy from. In addition, I want to take a chance and buy some rental property (even before I buy my own house) - this way, once rented, I create a monthly income for myself and a liability for someone else. The potentially

smart thing to do is buy a rental property, but what I

want to do is buy a new vehicle. My family tells me "you only live once"...which may be true - but do I also want to be richer or poorer in the long run given the economic trend of low wages, job uncertainty, and constant increase in prices? Which would you choose?

BE FREE